For generations, property has been one of Australia’s most trusted pathways to financial independence. From first-time investors purchasing a single investment property to experienced families building multi-generational portfolios, the Australian dream has often extended well beyond home ownership. It has been about creating lasting wealth.

Today, however, many investors are questioning whether that path is becoming increasingly difficult. A series of proposed and announced policy changes by the Federal Labor Government has sparked growing concern across the property industry, with many believing the rules of wealth creation are gradually being rewritten.

Supporters argue these reforms are designed to improve housing affordability and create a fairer tax system. Critics believe they are steadily increasing the burden on taxpayers and investors while doing little to address the fundamental issues driving Australia’s housing crisis.

Regardless of where one stands politically, one thing is becoming increasingly evident. Australia’s investment landscape is entering a period of significant change, and investors will need to become more strategic than ever before.

An Economy Under Pressure

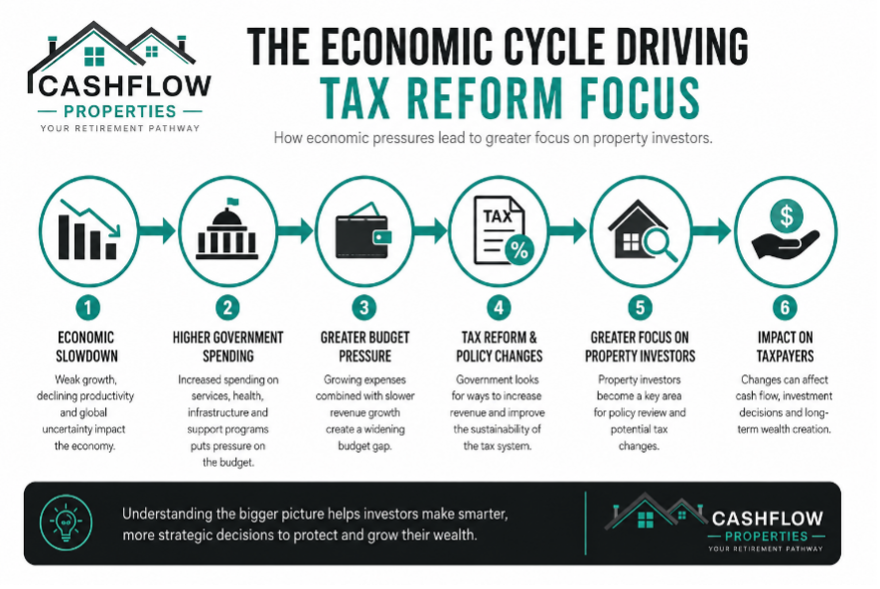

Australia’s economy is facing challenges on multiple fronts. Although the country has avoided a prolonged technical recession, economic growth has slowed considerably and many households are experiencing what economists describe as a “per capita recession,” where economic output per person has declined despite overall population growth.

Inflation has remained stubbornly above the Reserve Bank of Australia’s preferred range for an extended period, forcing interest rates to remain significantly higher than they were only a few years ago. At the same time, Australians continue to grapple with rising living costs, increasing mortgage repayments and reduced disposable income.

While government spending has remained elevated since the pandemic, budget pressures continue to grow. Every government must eventually balance increasing expenditure with sustainable revenue, and this has inevitably shifted attention towards taxation reform.

Many property analysts believe this changing economic backdrop explains why investment taxation has become one of the government’s major areas of focus.

Are Property Investors Becoming the Easy Target?

Rather than introducing broad-based tax increases across the entire population, governments often look for areas where revenue can be increased through targeted reforms.

Property investors have increasingly found themselves at the centre of this conversation.

While no single policy fundamentally changes the investment landscape overnight, many investors are becoming concerned about the cumulative impact of multiple reforms. It is not simply one proposal that creates uncertainty. It is the growing perception that each successive policy makes long-term wealth creation more challenging than it was for previous generations.

This uncertainty alone can influence investment decisions, often causing investors to delay purchases or reconsider expansion plans.

The Debate Around Negative Gearing

Negative gearing has long been one of the defining features of Australia’s property investment system. Under the current framework, eligible investors can generally offset investment losses against their taxable income, improving annual cash flow and making it easier to hold assets over the long term.

Proposed reforms have reignited debate around whether these benefits should continue in their current form.

Many investors fear that if deductions are deferred rather than received during ownership, they will effectively be financing a larger share of the investment themselves until the property is eventually sold. While the tax benefit may still exist, receiving it years later instead of annually could significantly affect cash flow, borrowing capacity and the ability to grow a portfolio.

Supporters of reform argue that limiting these concessions could improve housing affordability by reducing investor demand. Opponents counter that discouraging private investment may reduce the supply of rental housing at a time when vacancy rates are already near historic lows.

Changing the Role of Family Trusts

Family trusts have traditionally been one of the most effective vehicles for asset protection, succession planning and tax management.

The Government’s proposed taxation changes affecting discretionary trusts from July 2028 have generated considerable discussion among accountants, financial planners and business owners. Many families are now reviewing structures that have remained unchanged for years, recognising that strategies which worked in the past may no longer deliver the same outcomes in the future.

Rather than relying on standard ownership models, investors are increasingly seeking specialist advice to ensure their structures remain effective under evolving legislation.

Borrowing Through Super Could Become More Difficult

Another topic generating discussion within the investment community is the future of Limited Recourse Borrowing Arrangements (LRBAs) used by self-managed superannuation funds.

Although ban on purchasing residential property through LRBAs has been introduced, the possibility of tighter regulations has become part of broader policy discussions surrounding housing affordability and financial stability.

Whether these reforms ultimately eventuate remains uncertain. However, investors are recognising that policy risk itself has become another factor to consider when planning long-term investment strategies.

What Happens Next?

Perhaps the greatest concern among investors is not today’s reforms, but tomorrow’s possibilities.

Many are beginning to wonder what additional measures could emerge over the coming decade. Questions surrounding further borrowing restrictions, additional taxation reforms or even tighter controls on leveraging accumulated equity are becoming increasingly common within industry discussions.

There is currently no confirmed policy supporting many of these concerns. Nevertheless, uncertainty has a powerful influence on investor confidence, and markets rarely respond well when future rules appear unpredictable.

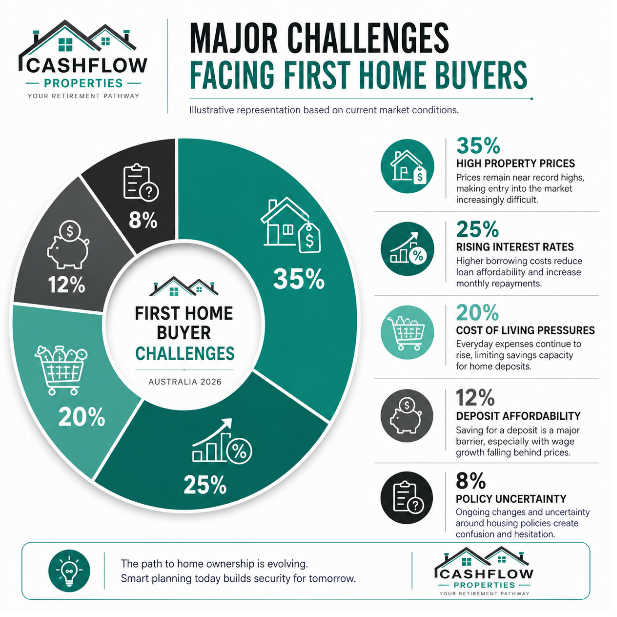

First Home Buyers Are Still Struggling

One of the primary objectives behind many housing reforms is to improve affordability for first home buyers. Yet despite ongoing policy initiatives, entering the property market remains an enormous challenge for many Australians.

National dwelling prices continue to sit near record highs, while elevated construction costs, persistent housing shortages and strong population growth continue to place upward pressure on prices.

Meanwhile, wage growth has struggled to keep pace with both inflation and housing costs, leaving many aspiring buyers feeling increasingly uncertain about when or even whether they will be able to purchase their first home.

Ironically, uncertainty affects first home buyers almost as much as investors. As policies continue to evolve, many buyers remain hesitant, worried about purchasing at the wrong time or facing further changes that could alter market conditions.

Wealth Creation Now Demands Greater Sophistication

The era of simply purchasing an investment property and allowing time to do the rest may be coming to an end.

Today’s investors face a far more complex environment where taxation, ownership structures, lending policies and legislative changes all play an increasingly important role in long-term outcomes.

Success is becoming less about buying more properties and more about making smarter decisions. Experienced investors are placing greater emphasis on structuring assets efficiently, maintaining healthy cash flow and ensuring their portfolios remain adaptable as government policy evolves.

Those who continue relying on strategies that worked twenty years ago may discover they are no longer sufficient in today’s regulatory environment.

Protecting Generational Wealth

As Australia’s property market evolves, protecting wealth has become just as important as creating it.

This means looking beyond individual property purchases and adopting a holistic investment strategy that considers taxation, succession planning, financing and long-term risk management. Building generational wealth is no longer simply about acquiring assets. It is about ensuring those assets remain protected and continue delivering value regardless of changing government policies.

Professional guidance from experienced accountants, mortgage specialists and property strategists has therefore become increasingly valuable. The right structure established today could make a significant difference over decades of investing.

Final Thoughts

Australia’s property market has always evolved alongside changing economic conditions, and government policy will inevitably continue to shape how Australians build wealth.

Whether the current reforms ultimately improve housing affordability or simply make investment more difficult remains a subject of considerable debate. What is undeniable, however, is that the rules are changing.

For investors, this is not necessarily the end of opportunity. Rather, it is a signal that success will increasingly belong to those who understand strategy, structure and long-term planning.

The future of wealth creation in Australia may not depend solely on buying the right property. It may depend on building the right framework around it.