The Australian property market is entering a phase that feels very different from the boom years many investors grew comfortable with. Rising interest rates, persistent inflation, and shifting affordability dynamics are forcing a reset in how investors think about growth, risk, and yield. The traditional playbook of buying detached houses on large blocks is being challenged, not because it no longer works, but because it is increasingly out of reach for the average investor.

As we move into 2026, the question is no longer simply “what grows fastest,” but rather “what remains accessible, rentable, and resilient in a high-cost environment.”

The Traditional Safe Bet- Detached Houses

For decades, most investors, particularly mum and dad investors, have leaned towards detached houses. The logic has always been grounded in one fundamental principle. Land appreciates over time, and houses typically come with a larger land component. This has historically delivered strong capital growth and long-term wealth creation.

There was also a time when this strategy was widely accessible. Investors could purchase a decent house on a reasonable block of land for under $500,000 in many parts of Australia. Investors like Bharat built portfolios during this phase by identifying growth corridors and leveraging affordability. That window has narrowed significantly. Property values have surged over the past five years, particularly in the detached housing segment.

The Affordability Crunch: A Structural Shift in the Market

The landscape today tells a very different story.

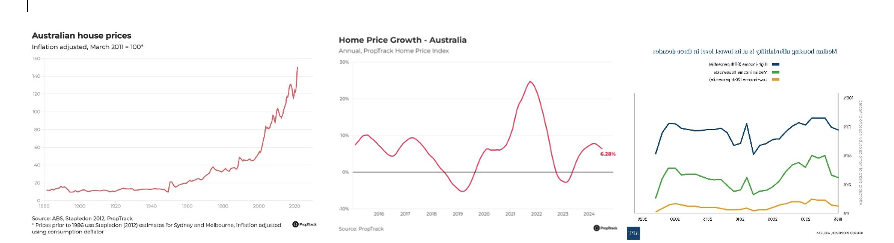

According to the CoreLogic Home Value Index, national dwelling values rose significantly between 2020 and 2024, with some regions recording growth of 30 to 40 percent over five years. This level of growth has pushed detached housing into a price bracket that is increasingly inaccessible for entry-level investors.

At the same time, the Reserve Bank of Australia has lifted interest rates multiple times to combat inflation, directly impacting borrowing capacity. Higher mortgage repayments mean that what an investor could borrow two years ago is no longer feasible today.

Add to this the rising cost of living and growing concerns around job security, and affordability has become the central theme of the 2026 market.

The Australian Bureau of Statistics has also highlighted that construction costs have surged due to inflationary pressures, labour shortages, and supply chain disruptions. Builders and developers are struggling to maintain margins, and trades are charging significantly more than they did just a few years ago.

The result is simple. New homes are becoming a distant dream for many buyers.

The Emerging Trend- Shift Towards Affordable Housing

As houses become less affordable, buyers and tenants are naturally shifting towards more accessible property types. This shift is not driven by preference alone but by necessity. The market is responding to what people can realistically afford rather than what they ideally want.

Why Affordable Villas and Townhouses Are Gaining Momentum

Affordable villas and townhouses, particularly those priced below $450,000 to $500,000, are emerging as strong performers in the current cycle. They offer a balance between affordability and functionality that aligns with present economic conditions.

These properties provide more space and privacy than apartments while remaining significantly more affordable than detached houses. This makes them highly attractive to both renters and first-time buyers, ensuring consistent demand.

Yield Matters More Than Ever

In a rising interest rate environment, rental yield has become a critical factor. Investors need properties that can support higher holding costs. Affordable villas and townhouses often deliver stronger yields compared to houses.

A practical example can be seen in Bharat’s portfolio. An investor purchased a villa in Cairns for approximately $260,000 and secured a rental income of around $390 per week. This demonstrates how lower entry prices combined with solid rental demand can create a sustainable investment.

The Importance of Low Strata and Small Complexes

Not all townhouses and villas will perform equally. The key is to focus on properties in small complexes with low strata fees. These properties offer lower ongoing costs, which improves net returns for investors while remaining attractive to tenants.

Buying Below Replacement Cost: A Strategic Advantage

One of the most compelling strategies in the current market is purchasing properties below replacement cost. With construction costs rising, it is often more expensive to build a new property than to buy an existing one.

This creates a built-in advantage. When you buy below replacement cost, you are effectively acquiring an asset that would cost more to recreate in today’s environment. Over time, this supports price stability and growth.

Investors like Bharat are actively targeting such opportunities, particularly in markets where prices have not yet fully reflected rising construction costs. This approach adds a layer of security to the investment while positioning it for future upside.

The Ripple Effect- Retirement and Budget Housing

Retirement villages: Where housing is still affordable

Another segment influencing the market is retirement villages. These properties are attracting downsizers due to their lower price points, allowing them to free up capital while maintaining a comfortable lifestyle.

As demand increases in this segment, it indirectly supports the broader affordable housing market. Villas and townhouses benefit from this shift, as they remain one of the most practical options for both downsizers and budget-conscious buyers.

Why Detached Houses May Lag in the Short Term

While detached houses will always remain a cornerstone of the property market, their short-term performance may be constrained. High entry prices limit the buyer pool, and reduced borrowing capacity further impacts demand.

Additionally, rental yields on houses are often lower relative to their value, increasing the financial burden on investors during periods of high interest rates. These factors may result in slower growth compared to more affordable property types.

The Investor Mindset Shift for 2026

The biggest shift required in 2026 is in mindset. The traditional focus on land value and long-term capital growth needs to be balanced with considerations such as affordability, yield, and demand resilience.

Investors need to align their strategies with current market realities rather than past performance trends.

Follow Affordability, Not Just Land Value

The Australian property market continues to evolve, and 2026 will reward those who understand the new demand drivers. Rising interest rates, inflation, and limited supply are reshaping buyer behaviour and investment opportunities.

Affordable villas and townhouses, particularly those under $500,000 with low strata costs and strong rental demand, are well positioned to outperform in this cycle. They align with what the majority of buyers and renters can afford, making them both practical and resilient investments.

For example, Bharat secured a cheap villa at $258,000, renting at $430 a week in Queensland for his client.

For investors willing to adapt, this shift presents a clear opportunity. The focus should no longer be solely on owning more land, but on owning the right type of property for the market conditions ahead.