For most Australians, the dream is simple. Buy a home, work hard, and pay it off as quickly as possible. The idea of becoming debt-free feels safe, responsible, and financially secure. As a result, many homeowners pour every spare dollar into reducing the mortgage on their principal place of residence (PPOR).

But here is the question many investors fail to ask:

Is aggressively paying off your home really the smartest path to wealth creation?

In today’s Australian property market, the answer is often no. The reality is that focusing only on reducing your home loan can sometimes slow down your long-term financial growth. Instead of making your money work harder, you may be locking your capital into a non-income-producing asset while missing valuable investment opportunities during your highest earning years.

At Cashflow Properties, the philosophy is different. Rather than rushing to eliminate debt early, the focus is on building strategic wealth first and using that wealth later to pay off the family home intelligently.

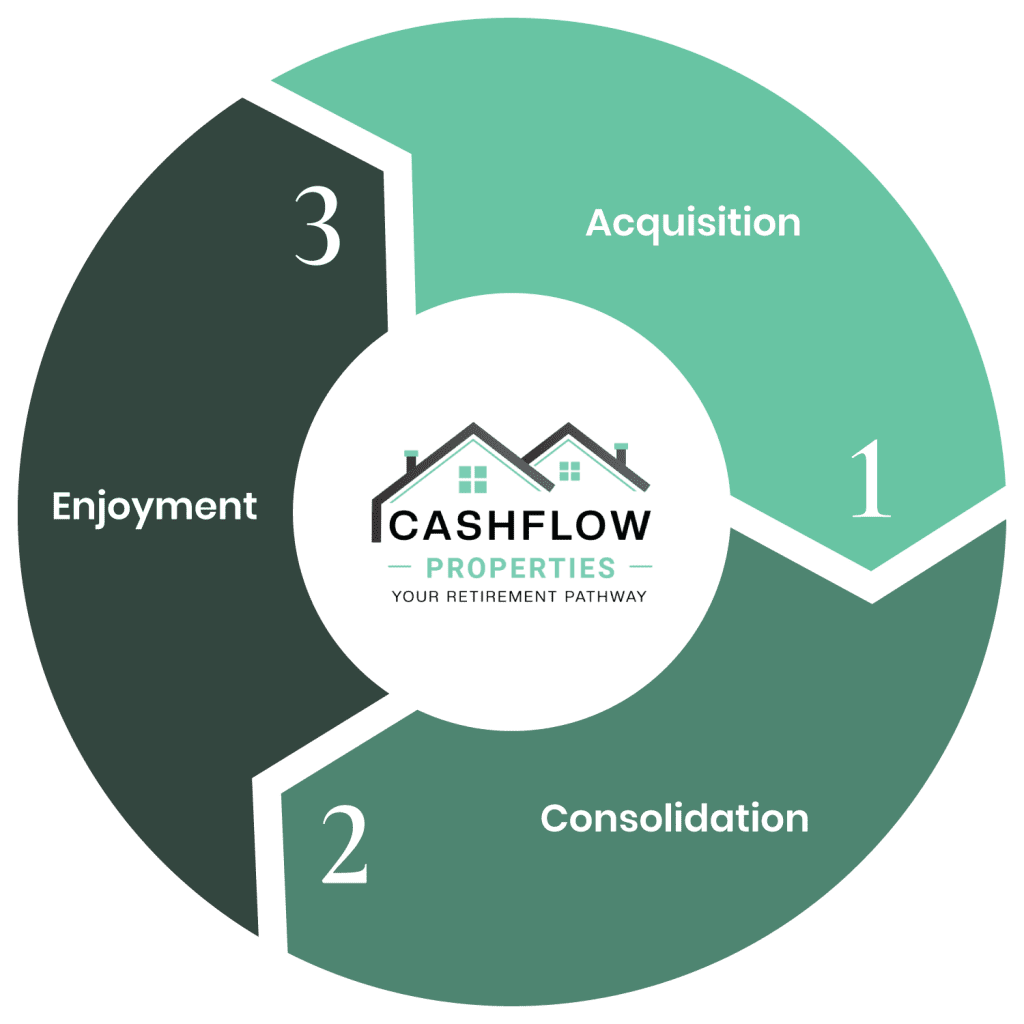

The model follows a simple but powerful cycle:

Acquire → Hold → Consolidate → Pay Off Your Home

Why Most Australians Focus Only on Paying Off Their Home

For decades, Australians have been taught that debt is dangerous and that a paid-off home equals financial success. While owning your home outright is certainly a milestone, the problem is that many people become so focused on eliminating their mortgage that they stop investing altogether.

Instead of acquiring assets that generate long-term growth, they dedicate every extra dollar toward reducing their home loan balance.

The issue is that your PPOR does not generate income. It does not produce rental cash flow, and in most cases, the interest on your home loan is not tax deductible.

Meanwhile, investment properties can provide:

- Rental income

- Capital growth

- Tax benefits

- Leverage opportunities

- Long-term equity creation

This is why many financially successful investors choose to build wealth first and pay down debt later.

The Australian Market Rewards Long-Term Property Holders

Australian property has historically rewarded investors who hold quality assets over long periods.

According to research reports, residential property values across Australia rose by 8.1% in 2023 alone, adding more than $500 billion to the nation’s housing market. Sydney, Brisbane, Perth, and Adelaide have continued to experience strong demand due to population growth, housing shortages, and migration trends.

At the same time, rental markets remain extremely tight.

Property Market economics reported that national rental vacancy rates stayed below 1.5% across many Australian capital cities throughout 2024, driving strong rental growth and improving investor cash flow.

These conditions create opportunities for investors who enter the market early and hold strategically selected properties.

The Power of Investing While You Are Young

One of the biggest advantages younger Australians have is borrowing capacity.

When you are young, employed, healthy, and earning a solid income, banks are generally more willing to lend. Your serviceability is stronger, your working years ahead are longer, and your ability to recover from market cycles is greater.

This is the stage where aggressive investing can create enormous long-term benefits.

Unfortunately, many people do the opposite. They buy a home, become obsessed with paying it off, and delay investing for years. By the time they feel “comfortable” enough to invest, property prices have already moved significantly higher, and borrowing power may have reduced due to age, lifestyle expenses, or family commitments.

This is why investing early matters. A property purchased in your 30s has far more time to grow than one purchased in your 50s.

The Cashflow Properties Model

The Cashflow Properties approach focuses on using time, leverage, and market cycles to create wealth strategically.

Step 1: Acquire

The first stage is acquisition.

Instead of concentrating solely on paying off the family home, investors direct surplus income toward purchasing affordable investment properties with strong rental demand and long-term growth potential.

The focus is not on luxury homes or emotionally driven purchases. It is about buying sensible, income-producing assets in markets where affordability and rental demand support long-term holding.

Every saved dollar becomes an opportunity to acquire another asset.

Step 2: Hold

The second stage is holding.

This is where patience becomes powerful. Rather than selling too early, investors hold their portfolio through a full property cycle, typically seven to ten years. During this time, several things happen simultaneously:

- Property values may appreciate

- Rents generally rise over time

- Loan balances gradually reduce

- Equity accumulates

- Tax deductions assist cash flow

Australia’s rental market continues to demonstrate the importance of holding income-producing assets. SQM Research reported that asking rents across major capitals increased substantially over recent years due to limited housing supply. This means well-selected investment properties can increasingly support themselves over time.

The key is affordability. This strategy is not about buying highly speculative properties that stretch your finances. It is about acquiring manageable investments where rising rents and long-term growth improve sustainability.

Focus on Overall Cash Flow, Not Just Debt Reduction

One major mindset shift investors need is understanding the difference between “good debt” and “bad debt.”

A home loan on your PPOR may provide emotional security, but it does not generate income. Investment debt, when attached to quality assets, can help create wealth over time. This is why successful investors focus on overall portfolio cash flow rather than simply reducing mortgage balances. A portfolio of seven to ten well-performing investment properties held across a growth cycle can create substantial equity and income potential. The objective is not to remain in debt forever. The objective is to use strategic debt to build assets first.

Step 3: Consolidate

This is where the strategy becomes truly powerful.

After holding properties through a full growth cycle of seven to ten years, investors can begin consolidating their portfolio. Rather than keeping every property forever, the idea is to strategically sell part of the portfolio and use the profits to reduce or eliminate non-deductible debt on the family home.

For example:

- Hold eight investment properties during the growth phase

- Sell four properties after substantial capital growth

- Use profits and equity to pay down the PPOR mortgage

- Retain four investment properties for continued income and long-term wealth

This creates a balance between debt reduction and asset retention.

Instead of spending decades slowly paying off a home with after-tax income, investors can potentially accelerate the process using capital growth generated by their investment portfolio.

That is working smarter, not harder.

Why This Strategy Is Not as Risky as People Think

Many Australians hear the idea of owning multiple investment properties and immediately assume it is dangerous.

The truth is that risk often comes from poor asset selection, overpaying, or lacking a long-term plan. When investors buy affordable properties with strong rental demand and sustainable cash flow, the strategy becomes far more manageable. Rising rents can help offset increasing interest rates over time. Australia’s ongoing housing shortage also continues to support rental demand across many regions.

According to the National Housing Finance and Investment Corporation, Australia is projected to face a significant housing supply shortfall over the coming years, which may continue placing upward pressure on rents.

The goal is controlled, strategic growth.

The Tax Advantages Investors Should Understand

Another important consideration is tax efficiency. Unlike a PPOR mortgage, investment property expenses may be tax deductible. Depending on your circumstances, investors may be able to claim:

- Loan interest

- Property management fees

- Depreciation

- Repairs and maintenance

- Insurance

- Council rates

These deductions can improve overall cash flow and reduce the holding burden.

While tax benefits should never be the sole reason for investing, they can support long-term portfolio sustainability when used correctly. Always seek advice from a qualified accountant or financial adviser before making financial decisions.

Paying Off Your Home Is Still the Goal

This strategy is not against owning your home outright. In fact, the ultimate objective is still financial freedom and a debt-free lifestyle.

The difference is in the approach. Rather than sacrificing decades of investment opportunities to pay off the home first, the Cashflow Properties model focuses on building assets aggressively during high-income years and then using accumulated equity to eliminate debt later. It is a strategy built around leverage, timing, cash flow, and long-term thinking.

Closing Thoughts

For many Australians, the safest path feels like aggressively paying off the family home as quickly as possible. But in reality, wealth creation often comes from owning appreciating assets, not simply reducing debt. By investing early, holding strategically, and consolidating intelligently, investors may create far greater financial flexibility over time.

The key lessons are simple:

- Use your younger earning years wisely

- Invest while borrowing capacity is strong

- Focus on affordable, income-producing assets

- Hold through market cycles

- Consolidate strategically later

- Use growth to eliminate non-deductible debt

For Example, our founder Bharat Patel used the same model to build his large property portfolio.

Property investing is not about becoming rich overnight. It is about building a long-term system that allows your assets to work for you. And sometimes, the fastest way to pay off your home is not by focusing only on your home at all.